Empower Your Retired Life: The Smart Method to Purchase a Reverse Home Mortgage

As retirement strategies, lots of individuals look for efficient strategies to boost their monetary freedom and wellness. Amongst these methods, a reverse mortgage arises as a viable alternative for property owners aged 62 and older, permitting them to take advantage of their home equity without the necessity of month-to-month payments. While this monetary tool uses several benefits, consisting of enhanced money flow and the prospective to cover crucial costs, it is crucial to comprehend the intricacies of the application procedure and key considerations entailed. The next actions might reveal how you can make a knowledgeable choice that could considerably impact your retirement years.

Understanding Reverse Home Mortgages

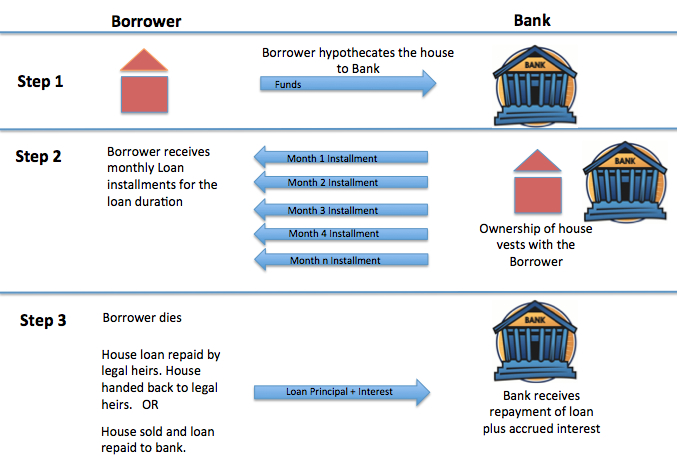

Comprehending reverse home mortgages can be crucial for property owners looking for monetary adaptability in retired life. A reverse home mortgage is an economic item that enables qualified house owners, commonly aged 62 and older, to transform a portion of their home equity right into money. Unlike standard home mortgages, where customers make monthly repayments to a lender, reverse home mortgages make it possible for house owners to get payments or a round figure while retaining possession of their residential or commercial property.

The amount offered with a reverse mortgage depends upon several aspects, consisting of the house owner's age, the home's worth, and existing rate of interest. Significantly, the car loan does not have actually to be settled till the home owner sells the home, moves out, or dies.

It is vital for prospective debtors to comprehend the effects of this financial item, consisting of the effect on estate inheritance, tax obligation factors to consider, and ongoing duties associated to residential property upkeep, tax obligations, and insurance. Furthermore, counseling sessions with accredited professionals are typically required to make certain that consumers totally understand the terms and problems of the funding. Generally, a complete understanding of reverse home loans can empower house owners to make educated choices about their economic future in retired life.

Benefits of a Reverse Mortgage

A reverse mortgage supplies a number of compelling benefits for qualified house owners, specifically those in retirement. This monetary tool allows elders to transform a part of their home equity right into money, supplying important funds without the requirement for month-to-month home mortgage repayments. The money gotten can be used for different functions, such as covering medical costs, making home renovations, or supplementing retired life revenue, therefore enhancing general monetary flexibility.

One substantial advantage of a reverse mortgage is that it does not call for repayment up until the property owner vacates, sells the home, or passes away - purchase reverse mortgage. This function allows retired people to preserve their lifestyle and meet unanticipated expenses without the concern of monthly settlements. Additionally, the funds gotten are commonly tax-free, permitting house owners to use their money without fear of tax ramifications

In addition, a reverse mortgage can supply comfort, understanding that it can serve as an economic safeguard during tough times. Home owners likewise keep possession of their homes, ensuring they can proceed staying in an acquainted atmosphere. Ultimately, a reverse home mortgage can be a strategic economic source, equipping retirees to handle their funds successfully while enjoying their gold years.

The Application Refine

Navigating the application procedure for a reverse home mortgage is a crucial step for homeowners considering this economic choice. The first phase includes evaluating qualification, which normally needs the house owner to be at the very least 62 years of ages, own the home outright or have a low home loan balance, and inhabit the home as their primary residence.

When eligibility is validated, house owners must undertake a counseling session with a HUD-approved therapist. This session makes sure that they fully comprehend the implications of a reverse home loan, consisting of the obligations involved. purchase reverse mortgage. After finishing counseling, candidates can proceed to collect required documents, including evidence of revenue, assets, and the home's worth

The following step involves sending an application to a lender, who will certainly assess the monetary and residential or commercial property credentials. An appraisal of the home will likewise be performed to determine its market price. If accepted, the lending institution will present finance terms, which should be evaluated very carefully.

Upon approval, the closing procedure follows, where final files are signed, and funds are paid out. Comprehending each stage of this application procedure can significantly enhance the property owner's self-confidence and decision-making pertaining to reverse home mortgages.

Key Considerations Prior To Purchasing

Purchasing a reverse mortgage is a significant financial choice that calls for cautious factor to consider of numerous vital variables. Initially, recognizing your eligibility is crucial. House owners need to be at least 62 years of ages, and the home needs to be their primary house. Reviewing your monetary needs and objectives is similarly essential; determine whether a reverse home mortgage lines up with your long-term strategies.

A reverse mortgage can influence your qualification for specific government advantages, such as Medicaid. By thoroughly evaluating these factors to consider, you can make an extra informed choice about whether a reverse home mortgage is the appropriate monetary approach for your retirement.

Maximizing Your Funds

When you have actually protected a reverse mortgage, properly taking care of the funds comes to be a priority. The versatility of a reverse home mortgage permits property owners to utilize the funds in various means, but critical preparation is important to maximize their advantages.

One essential approach is to develop a look at this web-site budget plan that outlines your month-to-month expenses and economic goals. By identifying needed expenses such as medical care, real estate tax, and home upkeep, you can assign funds as necessary to guarantee lasting sustainability. Additionally, think about using a part of the funds for financial investments that can generate income or value over time, such as dividend-paying supplies or mutual funds.

Another essential facet is to maintain an emergency fund. Alloting a reserve from your reverse home loan can aid cover unexpected expenses, giving peace of mind and financial security. Consult with a monetary expert to discover possible tax implications and exactly how to integrate reverse home loan funds right into your total retired life approach.

Inevitably, prudent management of reverse mortgage funds can enhance your monetary protection, permitting you to appreciate your retired life years without the anxiety of financial unpredictability. Cautious planning and notified decision-making will certainly make sure that your funds function successfully for you.

Verdict

Finally, a reverse mortgage presents a viable financial strategy for seniors looking for to boost their retired life experience. By converting home equity into available funds, individuals can address essential expenses and safe and secure added funds without incurring monthly settlements. Cautious consideration of the linked ramifications and terms is vital to make the most of benefits. Eventually, leveraging this monetary tool can promote higher independence and boost general lifestyle throughout retirement years.

Comprehending reverse home mortgages can be vital for homeowners looking for economic versatility in retired life. A reverse mortgage is a monetary item that permits eligible house owners, typically aged 62 and older, to transform a section of their home equity into money. Unlike typical home loans, where consumers make monthly repayments to a lending institution, reverse mortgages allow home owners to receive repayments or a swelling sum while preserving ownership of their residential or commercial property.

On the whole, an extensive understanding of reverse home loans can equip house owners to make enlightened choices regarding their monetary future in retirement.

Consult with a you could check here financial advisor to explore directory possible tax obligation effects and just how to incorporate reverse home loan funds right into your general retired life method.